As I sat in my small Boston apartment, surrounded by stacks of bills and financial documents, I realized that debt management strategies weren’t just about numbers – they were about freedom. I had always been fascinated by the world of finance, but it wasn’t until I found myself struggling to make ends meet that I truly understood the importance of taking control of my debt. The myth that debt management is only for those who are financially savvy is simply not true; with the right mindset and tools, anyone can conquer their debt and start building a stronger financial future.

In this article, I’ll share my personal story and provide you with practical advice on how to implement effective debt management strategies. You’ll learn how to prioritize your debts, create a budget that works for you, and make smart financial decisions that will help you achieve your goals. My goal is to empower you with the knowledge and confidence you need to take charge of your financial destiny, and I’m excited to share my insights with you. Whether you’re struggling to make payments or simply looking to improve your financial situation, this guide will provide you with the tools and inspiration you need to succeed.

Table of Contents

Guide Overview: What You'll Need

Total Time: several weeks to several months

Estimated Cost: $0 – $100

Difficulty Level: Intermediate

Tools Required

- Calculator (for budgeting)

- Spreadsheet software (for tracking expenses)

- Pen and paper (for note-taking)

Supplies & Materials

- Notebook or binder (for organizing financial documents)

- File folders (for categorizing expenses)

- Pencil and eraser (for making changes to budget)

Step-by-Step Instructions

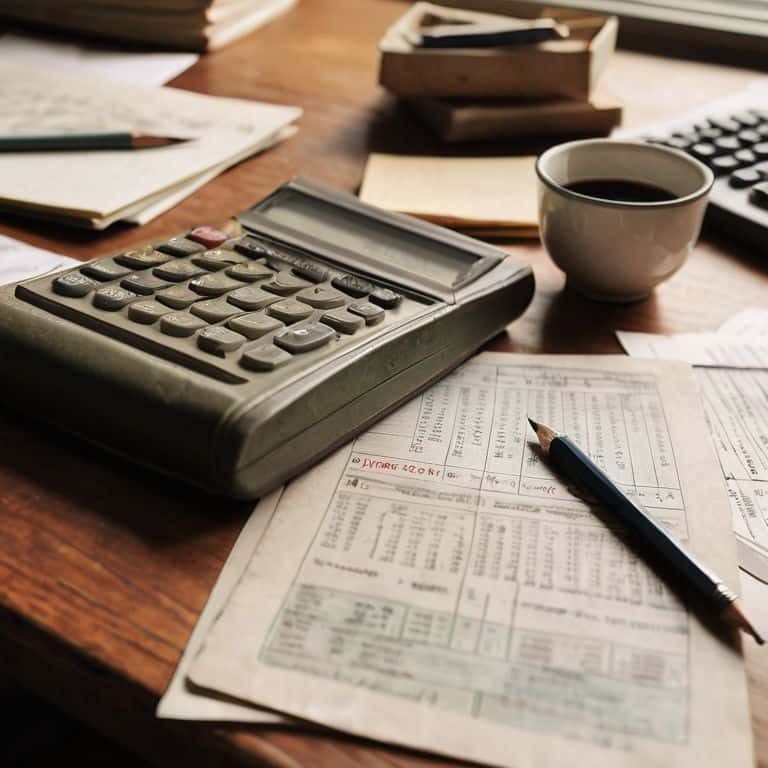

- 1. First, let’s start by assessing our financial situation and getting a clear picture of our debt. This involves gathering all the necessary documents, including credit card statements, loan papers, and any other debt-related paperwork. I like to use my vintage financial calculator to crunch the numbers and get a sense of the overall debt landscape. By doing so, we can identify areas where we can cut back on unnecessary expenses and allocate that money towards our debt.

- 2. Next, we need to prioritize our debts and focus on the ones with the highest interest rates first. This is often referred to as the “debt avalanche” method, where we tackle the most expensive debts first to save money on interest payments. My trusty vintage calculator comes in handy here, as I can quickly calculate the interest savings and stay motivated to keep pushing forward. By prioritizing our debts, we can make a significant impact on our overall financial health and start to see real progress.

- 3. Now that we have a plan in place, it’s time to create a budget that works for us, not against us. This involves tracking our income and expenses, and making adjustments as needed to ensure we’re allocating enough money towards our debt repayment. I’m a big fan of the 50/30/20 rule, where 50% of our income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment. By following this rule, we can achieve a sense of financial balance and make steady progress on our debt.

- 4. Another effective strategy is to consolidate our debts into a single, lower-interest loan or credit card. This can simplify our payments and save us money on interest charges. However, it’s essential to be cautious and only consider consolidation options that offer a lower interest rate and more favorable terms. My vintage calculator helps me run the numbers and determine whether consolidation is the right move for our specific situation. By consolidating our debts, we can streamline our finances and reduce stress.

- 5. In addition to consolidation, we can also consider negotiating with our creditors to see if they can offer any assistance. This might involve temporarily suspending payments, reducing interest rates, or waiving fees. It’s essential to approach these conversations with confidence and a clear understanding of our financial situation. I find that using my vintage calculator to prepare for these conversations helps me feel more empowered and in control.

- 6. As we make progress on our debt, it’s crucial to monitor our credit report and ensure it’s accurate. This involves checking for any errors or discrepancies that could be negatively impacting our credit score. By keeping a close eye on our credit report, we can protect our credit score and avoid any potential pitfalls.

- 7. Finally, let’s not forget the importance of celebrating our milestones and rewarding ourselves for our progress. This might involve treating ourselves to a small gift or simply taking time to reflect on how far we’ve come. My vintage calculator may not be able to calculate the value of our hard work and dedication, but it reminds me to stay focused and motivated on our journey to debt freedom.

Mastering Debt Management Strategies

As I sit here, surrounded by my collection of vintage financial calculators, I’m reminded that budgeting for debt reduction is a crucial step in taking control of one’s financial destiny. It’s about making conscious decisions about where your money goes, and ensuring that you’re allocating enough towards your debt. I’ve seen many individuals benefit from the snowball method, where they prioritize their debts by focusing on the smallest balance first, while still making minimum payments on other debts.

When it comes to debt, it’s essential to understand how it can impact your credit score. A poor credit score can make it challenging to secure loans or credit cards in the future, which is why it’s vital to be mindful of your credit utilization ratio. Some individuals may consider debt consolidation loans, but it’s crucial to weigh the pros and cons before making a decision. On the one hand, consolidation can simplify your payments, but on the other hand, it may not always be the most cost-effective solution.

To protect yourself from unexpected expenses, it’s a good idea to build an emergency fund. This fund will serve as a safety net, preventing you from going further into debt when unexpected expenses arise. Additionally, negotiating with creditors can be an effective way to reduce your debt burden. By communicating openly with your creditors, you may be able to come to a mutually beneficial agreement, such as a temporary reduction in payments or a waiver of late fees.

Conquering Debt With Budgeting Wisdom

As I sit here with my vintage financial calculator, I’m reminded that budgeting is the foundation of debt management. It’s the map that guides you through the financial wilderness, helping you navigate towards fiscal freedom. By prioritizing your expenses and allocating your resources wisely, you can create a budget that’s tailored to your unique situation. This isn’t about depriving yourself of life’s pleasures, but about making conscious choices that align with your financial goals.

With a well-crafted budget, you’ll be able to track your progress, identify areas for improvement, and make adjustments as needed. It’s a dynamic process that requires patience, discipline, and a willingness to learn. By mastering the art of budgeting, you’ll be empowered to take control of your debt and make steady progress towards a debt-free future.

Snowball vs Avalanche Choosing Your Path

As I sit here, surrounded by my collection of vintage financial calculators, I’m reminded of the age-old debate: Snowball vs Avalanche. Two approaches, each with its own merits, to tackle debt. The Snowball method, popularized by financial guru Dave Ramsey, involves paying off debts with the smallest balances first, while making minimum payments on larger debts. This approach provides a psychological boost as you quickly eliminate smaller debts. On the other hand, the Avalanche method focuses on paying off debts with the highest interest rates first, which can save you more money in interest over time.

I recall my travels to the financial district in New York, where I saw firsthand how these strategies play out in real life. Ultimately, the choice between Snowball and Avalanche depends on your personal financial situation and motivations. If you need a morale boost, Snowball might be the way to go. However, if you’re looking to save the most money in interest, Avalanche is likely your best bet.

5 Financial Wisdoms to Vanquish Your Debt

- Face Your Financial Foes: Gather all your debt information in one place, just like a general prepares for battle, to understand the scope of your debt and prioritize your attacks

- Deploy the 50/30/20 Shield: Allocate 50% of your income towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment to safeguard your financial future

- Choose Your Debt Dragon: Decide whether to tackle high-interest debts first (avalanche method) or smaller debts for quicker wins (snowball method), and stick to your chosen strategy

- Negotiate with Creditors: Don’t be afraid to reach out to your creditors to discuss possible interest rate reductions, payment plans, or temporary hardship programs – every little bit helps in the war against debt

- Maintain Your Financial Fortress: Regularly review and adjust your budget, ensure you’re taking advantage of any employer-matched retirement accounts, and consider automating your payments to secure your financial stronghold

Empowering Your Financial Future: 3 Key Takeaways

By adopting a hero’s mindset and tackling debt with courage and wisdom, you can transform your financial landscape and achieve fiscal freedom

Effective debt management strategies, such as budgeting wisdom and choosing between the snowball and avalanche methods, can be powerful tools in your quest to conquer debt

Remember, mastering debt management is not just about numbers – it’s about empowerment, and with the right knowledge and mindset, you can turn your financial story into one of triumph and adventure

A Financial Wisdom

Debt management is not just about numbers and budgets, it’s about crafting a narrative of financial freedom, where every payment is a chapter in the story of your economic liberation.

Olivia Peterson

Empowered to Thrive: A Debt-Free Tomorrow

As we conclude our journey through the realm of debt management strategies, let’s recap the essential tools we’ve gathered along the way. From mastering the art of budgeting to navigating the snowball vs avalanche debate, each step has been designed to empower you with the knowledge and confidence needed to tackle your debt head-on. By conquering debt with budgeting wisdom, you’ve taken the first crucial steps towards a financially freer you. Remember, debt management is not just about numbers; it’s about breaking free from the chains of financial stress and embracing a life of fiscal freedom.

Now, as you stand at the threshold of this new chapter in your financial journey, I urge you to embrace the courage and wisdom that has brought you this far. Your financial destiny is in your hands, and with the strategies and mindset you’ve adopted, you’re not just managing debt – you’re building a bridge to a brighter financial future. Keep moving forward, stay committed to your goals, and always remember that the power to transform your financial story lies within you. Together, let’s make finance an exciting journey, not a daunting obstacle.

Frequently Asked Questions

What are the most common debt management mistakes that people make and how can I avoid them?

As I reflect on my travels to historical financial districts, I’ve seen many fall into common debt traps. Two major mistakes are ignoring the debt avalanche and failing to account for variable expenses in their budget. Avoid these pitfalls by facing your debt head-on and being realistic about your spending habits – a lesson I’ll illustrate with my trusty vintage calculator.

How do I prioritize my debts when I have multiple creditors with different interest rates and payment due dates?

When faced with multiple creditors, I recommend prioritizing debts with the highest interest rates first, while still making minimum payments on other debts. This avalanche method can save you the most money in interest over time. My vintage calculator and I can help you crunch the numbers to create a personalized plan that suits your financial landscape.

Can debt management strategies like the snowball or avalanche method be combined with other financial tools, such as balance transfer credit cards or debt consolidation loans, for even greater effect?

I love exploring creative combinations to supercharge debt repayment. Yes, you can combine the snowball or avalanche method with balance transfer credit cards or debt consolidation loans for enhanced impact. For instance, using a 0% APR balance transfer card to tackle high-interest debt while applying the snowball method to smaller debts can be a winning strategy.